Trying to save tens of thousands of pounds can feel like a daunting prospect but we’re here to remind you that there is help out there when it comes to your deposit.

We want share some helpful ways in which you can boost the value of your deposit and make that dream of getting on the property ladder a reality.

Help to Buy

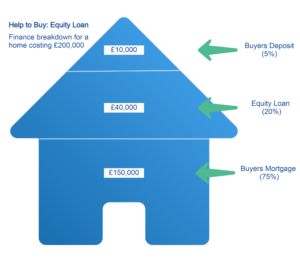

A Help to Buy equity loan is a great help if you’re a first-time buyer in the UK. An equity loan essentially supplements your deposit meaning you don’t have to save as much as originally thought. However you need to be mindful that any increase in the property value you will only see the proportionate increase of what you own. The Government only allow this scheme if the property you are purchasing is new build and the company who are selling the properties are part of the scheme. There are three financial components that make up the Help to Buy solution:

- Your deposit (5% minimum)

- Equity loan (loan 1, max 20% [London 40%])

- Repayment (Capital & Interest) Mortgage (loan 2, max 75% [London 55%])

Let’s assume a 5% deposit is set aside for example. We choose 5% because people with 10% (or more) set aside may get a better deal outside of the Help to Buy scheme. With this let’s imagine you buy a home for £200,000, have 5% deposit and take out the full 20% Equity Loan, you can see the breakdown in the image for this. Repayment of the loan will need to happen if you pay off the rest of your mortgage, sell your home or reach the end of your term (normally 25 years).

Shared ownership

This is another current way to make home ownership more affordable but should not be confused with joint or dual ownership. The purpose of this scheme is that you will buy part of your home and rent the rest.

It depends on the lender or landlord on what type of deal you get, but ultimately this should bring down the size of a deposit needed to be approved for a mortgage. Let’s say you were aiming for a 10% deposit on a house, because you are not purchasing the whole property the 10% mortgage is now 10% of a smaller amount. In some cases further down the line the option to purchase the rest of the property for full ownership could be available.

Buy with someone else

Two lots of savings is better than one, and if you have someone trustworthy in your life then a joint mortgage could be a way of getting on the property ladder more quickly.

It doesn’t have to be a partner or family member. Buying with friends can mean you can all save up more quickly to get the required deposit. Just make sure you talk about what happens if one of you wants to sell their share.

Buy somewhere that needs work

You might find your dream location is just too expensive for now. To get on the property ladder sooner you could find a cheaper property that needs some work doing, then you’ll have a property you can afford and possibly sell it for more money when that time comes.